本文最后更新于:2020年7月15日 中午

1、数据说明与预处理

本文选取的数据集来自于葡萄牙银行机构的营销活动,是以电话访谈的形式,根据访谈结果整合而成的。而电话访谈的最终目的,则是判断该用户是否会认购银行的产品——定期存款(term deposit)。因此,与该数据集对应的任务是分类任务,而分类目标是预测客户是(yes)否(no)认购定期存款,对应了数据集中的特征 y 。

数据集一共包含了41188个样例和17个特征,它们的含义如下表所示。

- I.客户个人信息

| 列名 | 含义说明 |

|---|---|

| age | 年龄 |

| job | 工作 |

| marital | 婚姻状况 |

| education | 受教育程度 |

| default | 是否有违约记录 |

| housing | 是否有住房贷款 |

| loan | 是否有个人贷款 |

| balance | 个人存款余额 |

- II.上一次电话营销的记录

| 列名 | 含义说明 |

|---|---|

| contact | 联系途径 |

| month | 月份 |

| day | 日期 |

| duration | 持续时间 |

- III.其他记录

| 列名 | 含义说明 |

|---|---|

| campaign | 在本次营销周期内与该客户的总通话次数 |

| pdays | 距离上一次通话的时间 |

| previous | 在过去的营销活动中与该客户的总通话次数 |

| poutcome | 上一次营销活动是否成功 |

- IV.目标特征

| 列名 | 含义说明 |

|---|---|

| y | 是否认购定期存款 |

引入包。

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

plt.rcParams['font.sans-serif']=['SimHei']

from sklearn.preprocessing import StandardScaler, OneHotEncoder, LabelEncoder

from sklearn.base import BaseEstimator, TransformerMixin

from sklearn.utils import check_array

from sklearn.pipeline import Pipeline, FeatureUnion

from sklearn.model_selection import train_test_split,cross_val_score,cross_val_predict

from sklearn.preprocessing import StandardScaler, LabelEncoder

from sklearn.linear_model import LogisticRegression

from sklearn.svm import SVC

from sklearn.neighbors import KNeighborsClassifier

from sklearn import tree

from sklearn.neural_network import MLPClassifier

from sklearn.ensemble import GradientBoostingClassifier

from sklearn.ensemble import RandomForestClassifier

from sklearn.naive_bayes import GaussianNB

from sklearn.metrics import roc_curve,roc_auc_score,confusion_matrix

import time

from scipy import sparse

# init_notebook_mode(connected=True)导入数据集,将包含所有数据的数据集命令为bank,通过前五行数据简要查看数据构成。

bank = pd.read_csv('./data/bank-full.csv',sep=';')

bank.head()输出:

| age | job | marital | education | default | balance | housing | loan | contact | day | month | duration | campaign | pdays | previous | poutcome | y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 58 | management | married | tertiary | no | 2143 | yes | no | unknown | 5 | may | 261 | 1 | -1 | 0 | unknown | no |

| 1 | 44 | technician | single | secondary | no | 29 | yes | no | unknown | 5 | may | 151 | 1 | -1 | 0 | unknown | no |

| 2 | 33 | entrepreneur | married | secondary | no | 2 | yes | yes | unknown | 5 | may | 76 | 1 | -1 | 0 | unknown | no |

| 3 | 47 | blue-collar | married | unknown | no | 1506 | yes | no | unknown | 5 | may | 92 | 1 | -1 | 0 | unknown | no |

| 4 | 33 | unknown | single | unknown | no | 1 | no | no | unknown | 5 | may | 198 | 1 | -1 | 0 | unknown | no |

接下来我们通过 describe() 和 info() 函数查看各列数据的分布情况。 这里我们首先用 describe() 函数分别观察数值型(numeric)特征的分布和类别型(categorical)特征的分布。 下边是数值型(numeric)特征的分布。

bank.describe() #数值型(numeric)特征数据分布| age | balance | day | duration | campaign | pdays | previous | |

|---|---|---|---|---|---|---|---|

| count | 45211.000000 | 45211.000000 | 45211.000000 | 45211.000000 | 45211.000000 | 45211.000000 | 45211.000000 |

| mean | 40.936210 | 1362.272058 | 15.806419 | 258.163080 | 2.763841 | 40.197828 | 0.580323 |

| std | 10.618762 | 3044.765829 | 8.322476 | 257.527812 | 3.098021 | 100.128746 | 2.303441 |

| min | 18.000000 | -8019.000000 | 1.000000 | 0.000000 | 1.000000 | -1.000000 | 0.000000 |

| 25% | 33.000000 | 72.000000 | 8.000000 | 103.000000 | 1.000000 | -1.000000 | 0.000000 |

| 50% | 39.000000 | 448.000000 | 16.000000 | 180.000000 | 2.000000 | -1.000000 | 0.000000 |

| 75% | 48.000000 | 1428.000000 | 21.000000 | 319.000000 | 3.000000 | -1.000000 | 0.000000 |

| max | 95.000000 | 102127.000000 | 31.000000 | 4918.000000 | 63.000000 | 871.000000 | 275.000000 |

接着我们观察类别型(categorical)特征的分布.

bank.describe(include=['O']) #类别型(categorical)特征数据分布输出:

| job | marital | education | default | housing | loan | contact | month | poutcome | y | |

|---|---|---|---|---|---|---|---|---|---|---|

| count | 45211 | 45211 | 45211 | 45211 | 45211 | 45211 | 45211 | 45211 | 45211 | 45211 |

| unique | 12 | 3 | 4 | 2 | 2 | 2 | 3 | 12 | 4 | 2 |

| top | blue-collar | married | secondary | no | yes | no | cellular | may | unknown | no |

| freq | 9732 | 27214 | 23202 | 44396 | 25130 | 37967 | 29285 | 13766 | 36959 | 39922 |

下面用info()观察缺失值的情况。

bank.info()输出:

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 45211 entries, 0 to 45210

Data columns (total 17 columns):

age 45211 non-null int64

job 45211 non-null object

marital 45211 non-null object

education 45211 non-null object

default 45211 non-null object

balance 45211 non-null int64

housing 45211 non-null object

loan 45211 non-null object

contact 45211 non-null object

day 45211 non-null int64

month 45211 non-null object

duration 45211 non-null int64

campaign 45211 non-null int64

pdays 45211 non-null int64

previous 45211 non-null int64

poutcome 45211 non-null object

y 45211 non-null object

dtypes: int64(7), object(10)

memory usage: 5.9+ MB通过观察 info() 函数给我们的结果,我们可以看出数据集中不存在缺失值。但是在此数据表中,部分数据以字符串 ‘unknown’ 形式存在于类别型特征里。使用如下代码查看类别型特征中 ‘unknown’ 的个数。

for col in bank.select_dtypes(include=['object']).columns: #筛选类型为object型数据,统计'unknown'个数

print(col+':',bank[bank[col]=='unknown'][col].count())输出:

job: 288

marital: 0

education: 1857

default: 0

housing: 0

loan: 0

contact: 13020

month: 0

poutcome: 36959

y: 0对于 ‘unknown’ 值的处理,我们会在3.1进行分析。

我们接下来查看样本类别分布情况。

bank['y'].value_counts()输出:

no 39922

yes 5289

Name: y, dtype: int64f, ax = plt.subplots(1,1, figsize=(4,4))

colors = ["#FA5858", "#64FE2E"]

labels ="no", "yes"

ax.set_title('是否认购定期存款', fontsize=16)

bank["y"].value_counts().plot.pie(explode=[0,0.25], autopct='%1.2f%%', ax=ax, shadow=True, colors=colors,labels=labels, fontsize=14, startangle=25)

plt.axis('off')

plt.show()2、探索性分析

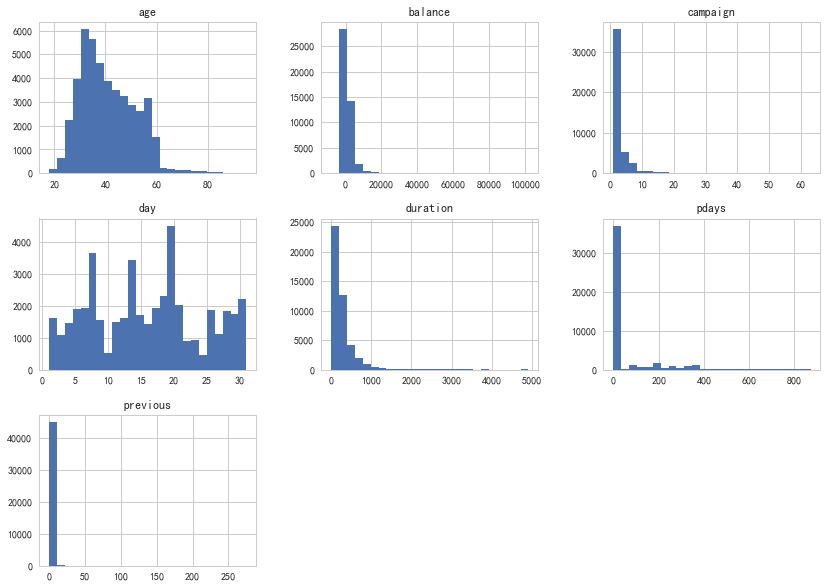

2.1 数值型特征的分布情况

我们首先通过DataFrame的 hist() 函数查看每个数值型特征的分布情况。值得一提的是,虽然我们是对整个数据表调用 hist() 函数,但是由于程序本身无法直观的理解类别型特征(因为它们以str形式存储),所以它们不会显示。

bank.hist(bins=25, figsize=(14,10))

plt.show()

2.2 类别型特征对结果的影响

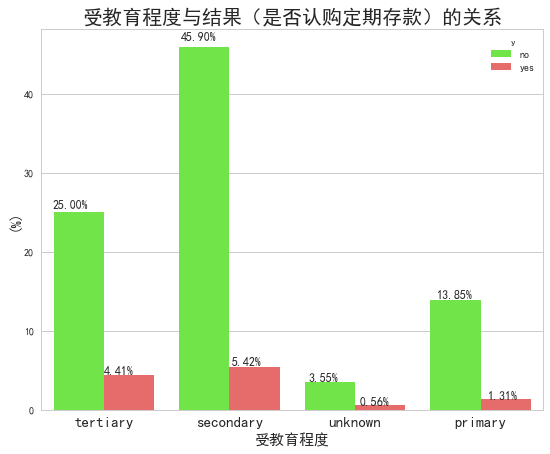

接下来我们查看正负样本点的不同之处。我们首先通过调用 barplot() 函数查看受教育程度 education 对结果(是否会定期存款)的影响。观察下图我们可以看出,受过高等教育(tertiary)和中等教育(secondary)的人群比只接受过初等教育的人更容易认购定期存款。

f, ax = plt.subplots(1,1, figsize=(9,7))

palette = ["#64FE2E", "#FA5858"]

sns.barplot(x="education", y="balance", hue="y", data=bank, palette=palette, estimator=lambda x: len(x) / len(bank) * 100)

for p in ax.patches:

ax.annotate('{:.2f}%'.format(p.get_height()),(p.get_x() * 1.02, p.get_height() * 1.02),fontsize=12)

ax.set_xticklabels(bank["education"].unique(), rotation=0, rotation_mode="anchor",fontsize=15)

ax.set_title("受教育程度与结果(是否认购定期存款)的关系",fontsize=20)

ax.set_xlabel("受教育程度",fontsize=15)

ax.set_ylabel("(%)",fontsize=15)

plt.show()

观察年龄随职业的分布,可以看出职业为 retired、self-employed两类左右两侧的分布有较明显的差别。在退休人群(retired)中,年龄越大的人越容易购买产品;个体经营(self-employed)群体中,年轻化的人更容易购买产品;观察年龄岁婚姻状况的分布,可以看出结婚的人(married)、离婚的人(divorced)相对于单身的人在是否会认购定期存款方面分布有明显的差异,前两类群体在高龄中越容易购买产品。

2.3 特征间的相关性

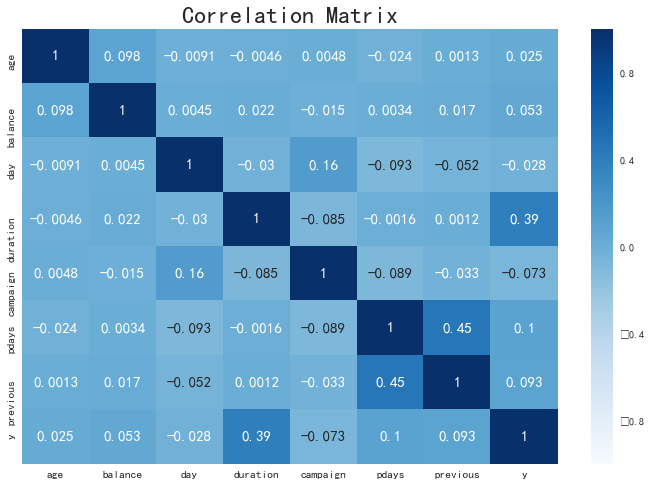

接下来我们通过关系矩阵查看各特征之间的关系,如下图所示。

fig, ax = plt.subplots(figsize=(12, 8))

bank['y'] = LabelEncoder().fit_transform(bank['y'])

numeric_bank = bank.select_dtypes(exclude="object")

corr_numeric = numeric_bank.corr()#关系矩阵,以矩阵形式存储

sns.heatmap(corr_numeric, annot=True, vmax=1, vmin=-1, cmap="Blues",annot_kws={"size":15})#热力图,即关系矩阵

ax.set_title("Correlation Matrix", fontsize=24)

ax.tick_params(axis='y',labelsize=11.5)

ax.tick_params(axis='x',labelsize=11.5)

plt.show()

观察上图我们可以看出通话时长( duration )与结果( y )相关性很高。这也可以很通俗地理解,如果通话时长 = 0,则y =0;如果通话时长越长,则客户越有可能接受银行的营销活动而认购定期存款(如下图所示)。

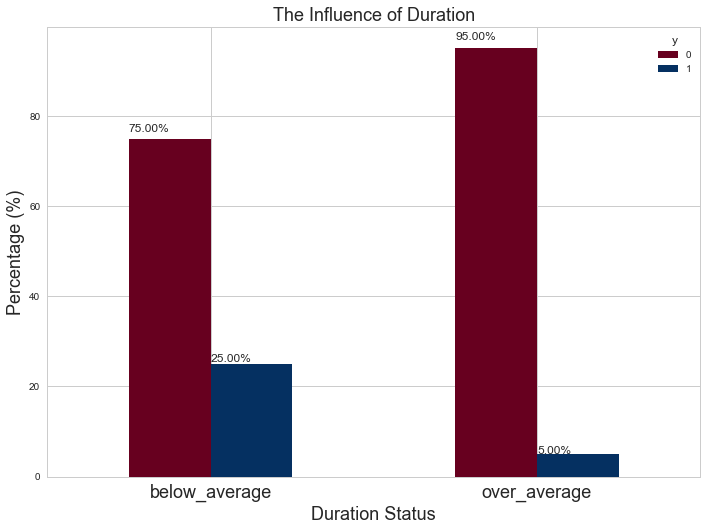

但是在实际中,这样做会有一个很大的问题,因为在执行通话之前你并不知道 duration 会是多久。但是,在通话结束后,显然你就会知道客户的意愿是认购还是拒绝。因此,应在模型训练前将这一特征删除。在下图,我们把 duration 按低于或高于其平均值分成了 below_average 和 over_average 两类,探究这两种情况下人们购买意愿的差异。根据我们的假设,属于 below_average 的人群中大多数人不会认购定期存款,属于 over_average 的人群中大多数人会选择认购定期存款。下方的代码生成的图像验证了我们的猜想。

sns.set(rc={'figure.figsize':(11.7,8.27)})

sns.set_style('whitegrid')

avg_duration = bank['duration'].mean()

#建立一个新特征以区分大于duration平均值的duration和小于均值的duration

bank["duration_status"] = np.nan

lst = [bank]

for col in lst:

col.loc[col["duration"] < avg_duration, "duration_status"] = "below_average"

col.loc[col["duration"] > avg_duration, "duration_status"] = "above_average"

#pd.crosstab另外一种分析双变量的方式,通过它可以得到两个变量之间的交叉信息,并作图。

pct_term = pd.crosstab(bank['duration_status'], bank['y']).apply(lambda r: round(r/r.sum(), 2) * 100, axis=1)

ax = pct_term.plot(kind='bar', stacked=False, cmap='RdBu')

ax.set_xticklabels(['below_average','over_average'], rotation=0, rotation_mode="anchor",fontsize=18)

plt.title("The Influence of Duration", fontsize=18)

plt.xlabel("Duration Status", fontsize=18);

plt.ylabel("Percentage (%)", fontsize=18)

for p in ax.patches:

ax.annotate('{:.2f}%'.format(p.get_height()), (p.get_x() , p.get_height() * 1.02))

plt.show()

bank.drop(['duration_status'], axis=1, inplace=True)

确实, over_average 的情况下就已经有95%的人选择认购定期存款了,这印证了我们的猜想。但是在本例中,我们不对duration做删除处理。大家可以尝试删除此特征执行同样的步骤,根据总结中最后一段提出的分别应用这两个模型进行预测的策略,应用到实际情况中。

3、数据预处理与特征工程

3.1 缺失值处理

在本文的开始我们提到过,虽然对所有数值型特征不存在缺失值,但是类别型特征中有以 'unknown' 形式存在的值,它们的统计结果如下,代码已在文章开头给出。

| 列名 | unknown值个数 |

|---|---|

| job | 288 |

| marital | 0 |

| education | 1857 |

| default | 0 |

| housing | 0 |

| loan | 0 |

| contact | 13020 |

| month | 0 |

| poutcom | 36959 |

| y | 0 |

缺失值处理通常有如下的方法:

- 对于

'unknown'值数量较少的特征,包括job和education,删除这些特征是缺失值('unknown')的行; - 如果预计该特征对于学习模型效果影响不大,而且在此例中缺失值都是类别型数据,可以对(

'unknown')值赋众数; - 可以使用数据完整的行作为训练集,以此来预测缺失值,特征

concact,poutcome的缺失值可以采取此法; - 我们也可以不处理它,使其保留

'unknown'的形式作为该特征的一种可能取值。

这里我们采取策略4,不进行处理。原因可以参考下一行代码,例如上一次营销活动的结果(poutcome)这一特征,大部分都是 'unknown' 值,其原因可以归结于这些客户没有经历上一次营销活动,是第一次参加本活动。当然,我们也可以结合策略1、3进行处理。

bank['poutcome'].value_counts()输出:

unknown 36959

failure 4901

other 1840

success 1511

Name: poutcome, dtype: int643.2 类型转换

我们知道原数据表中有数值型和类别型两种数据类型,但是机器学习模型只能读取数值型数据,因此我们需要进行类型的转换。通常我们可以先通过 LabelEncoder 再通过 OneHotEncoder 将str型数据转换成OneHot编码。但是这样每次只能操作一个类别型数据,函数写起来会比较麻烦。

在最新的开发者版本sklearn中提供了 CategoricalEncoder,它的好处是可以直接转换多列类别型数据。虽然当前版本没有提供,但是下面的代码块中供 了 CategoricalEncoder 的方法,只需要运行即可。

class CategoricalEncoder(BaseEstimator, TransformerMixin):

def __init__(self, encoding='onehot', categories='auto', dtype=np.float64,

handle_unknown='error'):

self.encoding = encoding

self.categories = categories

self.dtype = dtype

self.handle_unknown = handle_unknown

#fit方法与其他Encoder的使用方法一样

def fit(self, X, y=None):

"""Fit the CategoricalEncoder to X.

Parameters

----------

X : array-like, shape [n_samples, n_feature]

The data to determine the categories of each feature.

Returns

-------

self

"""

#编码有三种方式,按顺序分别为稀疏形式的独热编码,独热编码和序列编码。

if self.encoding not in ['onehot', 'onehot-dense', 'ordinal']:

template = ("encoding should be either 'onehot', 'onehot-dense' "

"or 'ordinal', got %s")

raise ValueError(template % self.handle_unknown)

if self.handle_unknown not in ['error', 'ignore']:

template = ("handle_unknown should be either 'error' or "

"'ignore', got %s")

raise ValueError(template % self.handle_unknown)

if self.encoding == 'ordinal' and self.handle_unknown == 'ignore':

raise ValueError("handle_unknown='ignore' is not supported for"

" encoding='ordinal'")

#处理特征

X = check_array(X, dtype=np.object, accept_sparse='csc', copy=True)

n_samples, n_features = X.shape

self._label_encoders_ = [LabelEncoder() for _ in range(n_features)]

#CategoricalEncoder的具体思路如下:

#先用LabelEncoder()转换成序列数据,再用OneHotEncoder()增添新的列转换成独热编码

#在fit阶段,只提取每一列的类别信息,为transform阶段做准备。

for i in range(n_features):

le = self._label_encoders_[i]

Xi = X[:, i]

if self.categories == 'auto':

le.fit(Xi)

else:

valid_mask = np.in1d(Xi, self.categories[i])

if not np.all(valid_mask):

if self.handle_unknown == 'error':

diff = np.unique(Xi[~valid_mask])

msg = ("Found unknown categories {0} in column {1}"

" during fit".format(diff, i))

raise ValueError(msg)

le.classes_ = np.array(np.sort(self.categories[i]))

self.categories_ = [le.classes_ for le in self._label_encoders_]

return self

def transform(self, X):

"""Transform X using one-hot encoding.

Parameters

----------

X : array-like, shape [n_samples, n_features]

The data to encode.

Returns

-------

X_out : sparse matrix or a 2-d array

Transformed input.

"""

#处理特征

X = check_array(X, accept_sparse='csc', dtype=np.object, copy=True)

n_samples, n_features = X.shape

X_int = np.zeros_like(X, dtype=np.int)

X_mask = np.ones_like(X, dtype=np.bool)

#转换类别型变量到独热编码的步骤

for i in range(n_features):

valid_mask = np.in1d(X[:, i], self.categories_[i])

if not np.all(valid_mask):

if self.handle_unknown == 'error':

diff = np.unique(X[~valid_mask, i])

msg = ("Found unknown categories {0} in column {1}"

" during transform".format(diff, i))

raise ValueError(msg)

else:

# Set the problematic rows to an acceptable value and

# continue `The rows are marked `X_mask` and will be

# removed later.

X_mask[:, i] = valid_mask

X[:, i][~valid_mask] = self.categories_[i][0]

X_int[:, i] = self._label_encoders_[i].transform(X[:, i])

#对于序列编码,直接处理后返回

if self.encoding == 'ordinal':

return X_int.astype(self.dtype, copy=False)

#以下是处理类别型数据的步骤

mask = X_mask.ravel()

n_values = [cats.shape[0] for cats in self.categories_]

n_values = np.array([0] + n_values)

indices = np.cumsum(n_values)

column_indices = (X_int + indices[:-1]).ravel()[mask]

row_indices = np.repeat(np.arange(n_samples, dtype=np.int32),

n_features)[mask]

data = np.ones(n_samples * n_features)[mask]

#默认是以稀疏矩阵的形式输出,节约内存

out = sparse.csc_matrix((data, (row_indices, column_indices)),

shape=(n_samples, indices[-1]),

dtype=self.dtype).tocsr()

#将稀疏矩阵转换成普通矩阵

if self.encoding == 'onehot-dense':

return out.toarray()

else:

return outbank[['job','marital']].head(5)输出:

| job | marital | |

|---|---|---|

| 0 | management | married |

| 1 | technician | single |

| 2 | entrepreneur | married |

| 3 | blue-collar | married |

| 4 | unknown | single |

a = CategoricalEncoder().fit_transform(bank[['job','marital']])

a.toarray()输出:

array([[0., 0., 0., ..., 0., 1., 0.],

[0., 0., 0., ..., 0., 0., 1.],

[0., 0., 1., ..., 0., 1., 0.],

...,

[0., 0., 0., ..., 0., 1., 0.],

[0., 1., 0., ..., 0., 1., 0.],

[0., 0., 1., ..., 0., 1., 0.]])a.shape输出:

(45211, 15)print(bank)输出:

| age | job | marital | education | default | balance | housing | loan | contact | day | month | duration | campaign | pdays | previous | poutcome | y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 58 | management | married | tertiary | no | 2143 | yes | no | unknown | 5 | may | 261 | 1 | -1 | 0 | unknown | 0 |

| 1 | 44 | technician | single | secondary | no | 29 | yes | no | unknown | 5 | may | 151 | 1 | -1 | 0 | unknown | 0 |

| 2 | 33 | entrepreneur | married | secondary | no | 2 | yes | yes | unknown | 5 | may | 76 | 1 | -1 | 0 | unknown | 0 |

| 3 | 47 | blue-collar | married | unknown | no | 1506 | yes | no | unknown | 5 | may | 92 | 1 | -1 | 0 | unknown | 0 |

| 4 | 33 | unknown | single | unknown | no | 1 | no | no | unknown | 5 | may | 198 | 1 | -1 | 0 | unknown | 0 |

| 5 | 35 | management | married | tertiary | no | 231 | yes | no | unknown | 5 | may | 139 | 1 | -1 | 0 | unknown | 0 |

| 6 | 28 | management | single | tertiary | no | 447 | yes | yes | unknown | 5 | may | 217 | 1 | -1 | 0 | unknown | 0 |

| 7 | 42 | entrepreneur | divorced | tertiary | yes | 2 | yes | no | unknown | 5 | may | 380 | 1 | -1 | 0 | unknown | 0 |

| 8 | 58 | retired | married | primary | no | 121 | yes | no | unknown | 5 | may | 50 | 1 | -1 | 0 | unknown | 0 |

| 9 | 43 | technician | single | secondary | no | 593 | yes | no | unknown | 5 | may | 55 | 1 | -1 | 0 | unknown | 0 |

| 10 | 41 | admin. | divorced | secondary | no | 270 | yes | no | unknown | 5 | may | 222 | 1 | -1 | 0 | unknown | 0 |

| 11 | 29 | admin. | single | secondary | no | 390 | yes | no | unknown | 5 | may | 137 | 1 | -1 | 0 | unknown | 0 |

| 12 | 53 | technician | married | secondary | no | 6 | yes | no | unknown | 5 | may | 517 | 1 | -1 | 0 | unknown | 0 |

| 13 | 58 | technician | married | unknown | no | 71 | yes | no | unknown | 5 | may | 71 | 1 | -1 | 0 | unknown | 0 |

| 14 | 57 | services | married | secondary | no | 162 | yes | no | unknown | 5 | may | 174 | 1 | -1 | 0 | unknown | 0 |

| 15 | 51 | retired | married | primary | no | 229 | yes | no | unknown | 5 | may | 353 | 1 | -1 | 0 | unknown | 0 |

| 16 | 45 | admin. | single | unknown | no | 13 | yes | no | unknown | 5 | may | 98 | 1 | -1 | 0 | unknown | 0 |

| 17 | 57 | blue-collar | married | primary | no | 52 | yes | no | unknown | 5 | may | 38 | 1 | -1 | 0 | unknown | 0 |

| 18 | 60 | retired | married | primary | no | 60 | yes | no | unknown | 5 | may | 219 | 1 | -1 | 0 | unknown | 0 |

| 19 | 33 | services | married | secondary | no | 0 | yes | no | unknown | 5 | may | 54 | 1 | -1 | 0 | unknown | 0 |

| 20 | 28 | blue-collar | married | secondary | no | 723 | yes | yes | unknown | 5 | may | 262 | 1 | -1 | 0 | unknown | 0 |

| 21 | 56 | management | married | tertiary | no | 779 | yes | no | unknown | 5 | may | 164 | 1 | -1 | 0 | unknown | 0 |

| 22 | 32 | blue-collar | single | primary | no | 23 | yes | yes | unknown | 5 | may | 160 | 1 | -1 | 0 | unknown | 0 |

| 23 | 25 | services | married | secondary | no | 50 | yes | no | unknown | 5 | may | 342 | 1 | -1 | 0 | unknown | 0 |

| 24 | 40 | retired | married | primary | no | 0 | yes | yes | unknown | 5 | may | 181 | 1 | -1 | 0 | unknown | 0 |

| 25 | 44 | admin. | married | secondary | no | -372 | yes | no | unknown | 5 | may | 172 | 1 | -1 | 0 | unknown | 0 |

| 26 | 39 | management | single | tertiary | no | 255 | yes | no | unknown | 5 | may | 296 | 1 | -1 | 0 | unknown | 0 |

| 27 | 52 | entrepreneur | married | secondary | no | 113 | yes | yes | unknown | 5 | may | 127 | 1 | -1 | 0 | unknown | 0 |

| 28 | 46 | management | single | secondary | no | -246 | yes | no | unknown | 5 | may | 255 | 2 | -1 | 0 | unknown | 0 |

| 29 | 36 | technician | single | secondary | no | 265 | yes | yes | unknown | 5 | may | 348 | 1 | -1 | 0 | unknown | 0 |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 45181 | 46 | blue-collar | married | secondary | no | 6879 | no | no | cellular | 15 | nov | 74 | 2 | 118 | 3 | failure | 0 |

| 45182 | 34 | technician | married | secondary | no | 133 | no | no | cellular | 15 | nov | 401 | 2 | 187 | 5 | success | 1 |

| 45183 | 70 | retired | married | primary | no | 324 | no | no | cellular | 15 | nov | 78 | 1 | 96 | 7 | success | 0 |

| 45184 | 63 | retired | married | secondary | no | 1495 | no | no | cellular | 16 | nov | 138 | 1 | 22 | 5 | success | 0 |

| 45185 | 60 | services | married | tertiary | no | 4256 | yes | no | cellular | 16 | nov | 200 | 1 | 92 | 4 | success | 1 |

| 45186 | 59 | unknown | married | unknown | no | 1500 | no | no | cellular | 16 | nov | 280 | 1 | 104 | 2 | failure | 0 |

| 45187 | 32 | services | single | secondary | no | 1168 | yes | no | cellular | 16 | nov | 411 | 1 | -1 | 0 | unknown | 1 |

| 45188 | 29 | management | single | secondary | no | 703 | yes | no | cellular | 16 | nov | 236 | 1 | 550 | 2 | success | 1 |

| 45189 | 25 | services | single | secondary | no | 199 | no | no | cellular | 16 | nov | 173 | 1 | 92 | 5 | failure | 0 |

| 45190 | 32 | blue-collar | married | secondary | no | 136 | no | no | cellular | 16 | nov | 206 | 1 | 188 | 3 | success | 1 |

| 45191 | 75 | retired | divorced | tertiary | no | 3810 | yes | no | cellular | 16 | nov | 262 | 1 | 183 | 1 | failure | 1 |

| 45192 | 29 | management | single | tertiary | no | 765 | no | no | cellular | 16 | nov | 238 | 1 | -1 | 0 | unknown | 1 |

| 45193 | 28 | self-employed | single | tertiary | no | 159 | no | no | cellular | 16 | nov | 449 | 2 | 33 | 4 | success | 1 |

| 45194 | 59 | management | married | tertiary | no | 138 | yes | yes | cellular | 16 | nov | 162 | 2 | 187 | 5 | failure | 0 |

| 45195 | 68 | retired | married | secondary | no | 1146 | no | no | cellular | 16 | nov | 212 | 1 | 187 | 6 | success | 1 |

| 45196 | 25 | student | single | secondary | no | 358 | no | no | cellular | 16 | nov | 330 | 1 | -1 | 0 | unknown | 1 |

| 45197 | 36 | management | single | secondary | no | 1511 | yes | no | cellular | 16 | nov | 270 | 1 | -1 | 0 | unknown | 1 |

| 45198 | 37 | management | married | tertiary | no | 1428 | no | no | cellular | 16 | nov | 333 | 2 | -1 | 0 | unknown | 0 |

| 45199 | 34 | blue-collar | single | secondary | no | 1475 | yes | no | cellular | 16 | nov | 1166 | 3 | 530 | 12 | other | 0 |

| 45200 | 38 | technician | married | secondary | no | 557 | yes | no | cellular | 16 | nov | 1556 | 4 | -1 | 0 | unknown | 1 |

| 45201 | 53 | management | married | tertiary | no | 583 | no | no | cellular | 17 | nov | 226 | 1 | 184 | 4 | success | 1 |

| 45202 | 34 | admin. | single | secondary | no | 557 | no | no | cellular | 17 | nov | 224 | 1 | -1 | 0 | unknown | 1 |

| 45203 | 23 | student | single | tertiary | no | 113 | no | no | cellular | 17 | nov | 266 | 1 | -1 | 0 | unknown | 1 |

| 45204 | 73 | retired | married | secondary | no | 2850 | no | no | cellular | 17 | nov | 300 | 1 | 40 | 8 | failure | 1 |

| 45205 | 25 | technician | single | secondary | no | 505 | no | yes | cellular | 17 | nov | 386 | 2 | -1 | 0 | unknown | 1 |

| 45206 | 51 | technician | married | tertiary | no | 825 | no | no | cellular | 17 | nov | 977 | 3 | -1 | 0 | unknown | 1 |

| 45207 | 71 | retired | divorced | primary | no | 1729 | no | no | cellular | 17 | nov | 456 | 2 | -1 | 0 | unknown | 1 |

| 45208 | 72 | retired | married | secondary | no | 5715 | no | no | cellular | 17 | nov | 1127 | 5 | 184 | 3 | success | 1 |

| 45209 | 57 | blue-collar | married | secondary | no | 668 | no | no | telephone | 17 | nov | 508 | 4 | -1 | 0 | unknown | 0 |

| 45210 | 37 | entrepreneur | married | secondary | no | 2971 | no | no | cellular | 17 | nov | 361 | 2 | 188 | 11 | other | 0 |

45211 rows × 17 columns

#DataFrameSelector类的作用是从DataFrame中选取特定的列,以便后续pipeline的便捷性。

class DataFrameSelector(BaseEstimator, TransformerMixin):

def __init__(self, attribute_names):

self.attribute_names = attribute_names

def fit(self, X, y=None):

return self

def transform(self, X):

return X[self.attribute_names]Python的 sklearn.pipeline.Pipeline() 函数可以把多个“处理数据的节点”按顺序打包在一起,数据在前一个节点处理之后的结果,转到下一个节点处理。当训练样本数据送进 Pipeline 进行处理时, 它会逐个调用节点的 fit() 和 transform() 方法,然后用最后一个节点的 fit() 方法来拟合数据。

对于数值型特征,我们对它用 StandardScaler() 进行标准化,对于类别型特征,我们用 CategoricalEncoder(encoding='onehot-dense') 进行OneHot编码。

# 制作管道

# #对数值型特征处理

numerical_pipeline = Pipeline([

("select_numeric", DataFrameSelector(["age", "balance", "day", "campaign", "pdays", "previous","duration"])),

("std_scaler", StandardScaler()),

])

#对类别型特征处理

categorical_pipeline = Pipeline([

("select_cat", DataFrameSelector(["job", "education", "marital", "default", "housing", "loan", "contact", "month","poutcome"])),

("cat_encoder", CategoricalEncoder(encoding='onehot-dense'))

])

#统一管道

preprocess_pipeline = FeatureUnion(transformer_list=[

("numerical_pipeline", numerical_pipeline),

("categorical_pipeline", categorical_pipeline),

])4、模型训练

4.1 数据集划分

# 划分X和y,以及训练集与测试集

X=bank.drop(['y'], axis=1)

y=bank['y']

print(X)输出:

| age | job | marital | education | default | balance | housing | loan | contact | day | month | duration | campaign | pdays | previous | poutcome | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 58 | management | married | tertiary | no | 2143 | yes | no | unknown | 5 | may | 261 | 1 | -1 | 0 | unknown |

| 1 | 44 | technician | single | secondary | no | 29 | yes | no | unknown | 5 | may | 151 | 1 | -1 | 0 | unknown |

| 2 | 33 | entrepreneur | married | secondary | no | 2 | yes | yes | unknown | 5 | may | 76 | 1 | -1 | 0 | unknown |

| 3 | 47 | blue-collar | married | unknown | no | 1506 | yes | no | unknown | 5 | may | 92 | 1 | -1 | 0 | unknown |

| 4 | 33 | unknown | single | unknown | no | 1 | no | no | unknown | 5 | may | 198 | 1 | -1 | 0 | unknown |

| 5 | 35 | management | married | tertiary | no | 231 | yes | no | unknown | 5 | may | 139 | 1 | -1 | 0 | unknown |

| 6 | 28 | management | single | tertiary | no | 447 | yes | yes | unknown | 5 | may | 217 | 1 | -1 | 0 | unknown |

| 7 | 42 | entrepreneur | divorced | tertiary | yes | 2 | yes | no | unknown | 5 | may | 380 | 1 | -1 | 0 | unknown |

| 8 | 58 | retired | married | primary | no | 121 | yes | no | unknown | 5 | may | 50 | 1 | -1 | 0 | unknown |

| 9 | 43 | technician | single | secondary | no | 593 | yes | no | unknown | 5 | may | 55 | 1 | -1 | 0 | unknown |

| 10 | 41 | admin. | divorced | secondary | no | 270 | yes | no | unknown | 5 | may | 222 | 1 | -1 | 0 | unknown |

| 11 | 29 | admin. | single | secondary | no | 390 | yes | no | unknown | 5 | may | 137 | 1 | -1 | 0 | unknown |

| 12 | 53 | technician | married | secondary | no | 6 | yes | no | unknown | 5 | may | 517 | 1 | -1 | 0 | unknown |

| 13 | 58 | technician | married | unknown | no | 71 | yes | no | unknown | 5 | may | 71 | 1 | -1 | 0 | unknown |

| 14 | 57 | services | married | secondary | no | 162 | yes | no | unknown | 5 | may | 174 | 1 | -1 | 0 | unknown |

| 15 | 51 | retired | married | primary | no | 229 | yes | no | unknown | 5 | may | 353 | 1 | -1 | 0 | unknown |

| 16 | 45 | admin. | single | unknown | no | 13 | yes | no | unknown | 5 | may | 98 | 1 | -1 | 0 | unknown |

| 17 | 57 | blue-collar | married | primary | no | 52 | yes | no | unknown | 5 | may | 38 | 1 | -1 | 0 | unknown |

| 18 | 60 | retired | married | primary | no | 60 | yes | no | unknown | 5 | may | 219 | 1 | -1 | 0 | unknown |

| 19 | 33 | services | married | secondary | no | 0 | yes | no | unknown | 5 | may | 54 | 1 | -1 | 0 | unknown |

| 20 | 28 | blue-collar | married | secondary | no | 723 | yes | yes | unknown | 5 | may | 262 | 1 | -1 | 0 | unknown |

| 21 | 56 | management | married | tertiary | no | 779 | yes | no | unknown | 5 | may | 164 | 1 | -1 | 0 | unknown |

| 22 | 32 | blue-collar | single | primary | no | 23 | yes | yes | unknown | 5 | may | 160 | 1 | -1 | 0 | unknown |

| 23 | 25 | services | married | secondary | no | 50 | yes | no | unknown | 5 | may | 342 | 1 | -1 | 0 | unknown |

| 24 | 40 | retired | married | primary | no | 0 | yes | yes | unknown | 5 | may | 181 | 1 | -1 | 0 | unknown |

| 25 | 44 | admin. | married | secondary | no | -372 | yes | no | unknown | 5 | may | 172 | 1 | -1 | 0 | unknown |

| 26 | 39 | management | single | tertiary | no | 255 | yes | no | unknown | 5 | may | 296 | 1 | -1 | 0 | unknown |

| 27 | 52 | entrepreneur | married | secondary | no | 113 | yes | yes | unknown | 5 | may | 127 | 1 | -1 | 0 | unknown |

| 28 | 46 | management | single | secondary | no | -246 | yes | no | unknown | 5 | may | 255 | 2 | -1 | 0 | unknown |

| 29 | 36 | technician | single | secondary | no | 265 | yes | yes | unknown | 5 | may | 348 | 1 | -1 | 0 | unknown |

| … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … | … |

| 45181 | 46 | blue-collar | married | secondary | no | 6879 | no | no | cellular | 15 | nov | 74 | 2 | 118 | 3 | failure |

| 45182 | 34 | technician | married | secondary | no | 133 | no | no | cellular | 15 | nov | 401 | 2 | 187 | 5 | success |

| 45183 | 70 | retired | married | primary | no | 324 | no | no | cellular | 15 | nov | 78 | 1 | 96 | 7 | success |

| 45184 | 63 | retired | married | secondary | no | 1495 | no | no | cellular | 16 | nov | 138 | 1 | 22 | 5 | success |

| 45185 | 60 | services | married | tertiary | no | 4256 | yes | no | cellular | 16 | nov | 200 | 1 | 92 | 4 | success |

| 45186 | 59 | unknown | married | unknown | no | 1500 | no | no | cellular | 16 | nov | 280 | 1 | 104 | 2 | failure |

| 45187 | 32 | services | single | secondary | no | 1168 | yes | no | cellular | 16 | nov | 411 | 1 | -1 | 0 | unknown |

| 45188 | 29 | management | single | secondary | no | 703 | yes | no | cellular | 16 | nov | 236 | 1 | 550 | 2 | success |

| 45189 | 25 | services | single | secondary | no | 199 | no | no | cellular | 16 | nov | 173 | 1 | 92 | 5 | failure |

| 45190 | 32 | blue-collar | married | secondary | no | 136 | no | no | cellular | 16 | nov | 206 | 1 | 188 | 3 | success |

| 45191 | 75 | retired | divorced | tertiary | no | 3810 | yes | no | cellular | 16 | nov | 262 | 1 | 183 | 1 | failure |

| 45192 | 29 | management | single | tertiary | no | 765 | no | no | cellular | 16 | nov | 238 | 1 | -1 | 0 | unknown |

| 45193 | 28 | self-employed | single | tertiary | no | 159 | no | no | cellular | 16 | nov | 449 | 2 | 33 | 4 | success |

| 45194 | 59 | management | married | tertiary | no | 138 | yes | yes | cellular | 16 | nov | 162 | 2 | 187 | 5 | failure |

| 45195 | 68 | retired | married | secondary | no | 1146 | no | no | cellular | 16 | nov | 212 | 1 | 187 | 6 | success |

| 45196 | 25 | student | single | secondary | no | 358 | no | no | cellular | 16 | nov | 330 | 1 | -1 | 0 | unknown |

| 45197 | 36 | management | single | secondary | no | 1511 | yes | no | cellular | 16 | nov | 270 | 1 | -1 | 0 | unknown |

| 45198 | 37 | management | married | tertiary | no | 1428 | no | no | cellular | 16 | nov | 333 | 2 | -1 | 0 | unknown |

| 45199 | 34 | blue-collar | single | secondary | no | 1475 | yes | no | cellular | 16 | nov | 1166 | 3 | 530 | 12 | other |

| 45200 | 38 | technician | married | secondary | no | 557 | yes | no | cellular | 16 | nov | 1556 | 4 | -1 | 0 | unknown |

| 45201 | 53 | management | married | tertiary | no | 583 | no | no | cellular | 17 | nov | 226 | 1 | 184 | 4 | success |

| 45202 | 34 | admin. | single | secondary | no | 557 | no | no | cellular | 17 | nov | 224 | 1 | -1 | 0 | unknown |

| 45203 | 23 | student | single | tertiary | no | 113 | no | no | cellular | 17 | nov | 266 | 1 | -1 | 0 | unknown |

| 45204 | 73 | retired | married | secondary | no | 2850 | no | no | cellular | 17 | nov | 300 | 1 | 40 | 8 | failure |

| 45205 | 25 | technician | single | secondary | no | 505 | no | yes | cellular | 17 | nov | 386 | 2 | -1 | 0 | unknown |

| 45206 | 51 | technician | married | tertiary | no | 825 | no | no | cellular | 17 | nov | 977 | 3 | -1 | 0 | unknown |

| 45207 | 71 | retired | divorced | primary | no | 1729 | no | no | cellular | 17 | nov | 456 | 2 | -1 | 0 | unknown |

| 45208 | 72 | retired | married | secondary | no | 5715 | no | no | cellular | 17 | nov | 1127 | 5 | 184 | 3 | success |

| 45209 | 57 | blue-collar | married | secondary | no | 668 | no | no | telephone | 17 | nov | 508 | 4 | -1 | 0 | unknown |

| 45210 | 37 | entrepreneur | married | secondary | no | 2971 | no | no | cellular | 17 | nov | 361 | 2 | 188 | 11 | other |

45211 rows × 16 columns

X = preprocess_pipeline.fit_transform(X)

X_train,X_test,y_train,y_test=train_test_split(X,y,test_size=0.2, random_state=44)

print(X)输出:

array([[ 1.60696496, 0.25641925, -1.29847633, ..., 0. ,

0. , 1. ],

[ 0.28852927, -0.43789469, -1.29847633, ..., 0. ,

0. , 1. ],

[-0.74738448, -0.44676247, -1.29847633, ..., 0. ,

0. , 1. ],

...,

[ 2.92540065, 1.42959305, 0.14341818, ..., 0. ,

1. , 0. ],

[ 1.51279098, -0.22802402, 0.14341818, ..., 0. ,

0. , 1. ],

[-0.37068857, 0.52836436, 0.14341818, ..., 1. ,

0. , 0. ]])preprocess_bank = pd.DataFrame(X)

preprocess_bank.head(5)输出:

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | … | 41 | 42 | 43 | 44 | 45 | 46 | 47 | 48 | 49 | 50 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.606965 | 0.256419 | -1.298476 | -0.569351 | -0.411453 | -0.25194 | 0.011016 | 0.0 | 0.0 | 0.0 | … | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| 1 | 0.288529 | -0.437895 | -1.298476 | -0.569351 | -0.411453 | -0.25194 | -0.416127 | 0.0 | 0.0 | 0.0 | … | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| 2 | -0.747384 | -0.446762 | -1.298476 | -0.569351 | -0.411453 | -0.25194 | -0.707361 | 0.0 | 0.0 | 1.0 | … | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| 3 | 0.571051 | 0.047205 | -1.298476 | -0.569351 | -0.411453 | -0.25194 | -0.645231 | 0.0 | 1.0 | 0.0 | … | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| 4 | -0.747384 | -0.447091 | -1.298476 | -0.569351 | -0.411453 | -0.25194 | -0.233620 | 0.0 | 0.0 | 0.0 | … | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

5 rows × 51 columns

bank.head(5)输出:

| age | job | marital | education | default | balance | housing | loan | contact | day | month | duration | campaign | pdays | previous | poutcome | y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 58 | management | married | tertiary | no | 2143 | yes | no | unknown | 5 | may | 261 | 1 | -1 | 0 | unknown | 0 |

| 1 | 44 | technician | single | secondary | no | 29 | yes | no | unknown | 5 | may | 151 | 1 | -1 | 0 | unknown | 0 |

| 2 | 33 | entrepreneur | married | secondary | no | 2 | yes | yes | unknown | 5 | may | 76 | 1 | -1 | 0 | unknown | 0 |

| 3 | 47 | blue-collar | married | unknown | no | 1506 | yes | no | unknown | 5 | may | 92 | 1 | -1 | 0 | unknown | 0 |

| 4 | 33 | unknown | single | unknown | no | 1 | no | no | unknown | 5 | may | 198 | 1 | -1 | 0 | unknown | 0 |

4.2 模型构建

t_diff=[]

逻辑回归

log_reg = LogisticRegression()

t_start = time.clock()#通过time记录

log_scores = cross_val_score(log_reg, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

log_reg_mean = log_scores.mean()

支持向量机

svc_clf = SVC()

t_start = time.clock()

svc_scores = cross_val_score(svc_clf, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

svc_mean = svc_scores.mean()

k邻近

knn_clf = KNeighborsClassifier()

t_start = time.clock()

knn_scores = cross_val_score(knn_clf, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

knn_mean = knn_scores.mean()

决策树

tree_clf = tree.DecisionTreeClassifier()

t_start = time.clock()

tree_scores = cross_val_score(tree_clf, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

tree_mean = tree_scores.mean()

梯度提升树

grad_clf = GradientBoostingClassifier()

t_start = time.clock()

grad_scores = cross_val_score(grad_clf, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

grad_mean = grad_scores.mean()

随机森林

rand_clf = RandomForestClassifier()

t_start = time.clock()

rand_scores = cross_val_score(rand_clf, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

rand_mean = rand_scores.mean()

神经网络

neural_clf = MLPClassifier(alpha=0.01)

t_start = time.clock()

neural_scores = cross_val_score(neural_clf, X_train, y_train, cv=3, scoring=’roc_auc’)

t_end = time.clock()

t_diff.append((t_end - t_start))

neural_mean = neural_scores.mean()

朴素贝叶斯

nav_clf = GaussianNB()

t_start = time.clock()

nav_scores = cross_val_score(nav_clf, X_train, y_train, cv=3, scoring='roc_auc')

t_end = time.clock()

t_diff.append((t_end - t_start))

nav_mean = neural_scores.mean()

d = {'Classifiers': ['Logistic Reg.', 'SVC', 'KNN', 'Dec Tree', 'Grad B CLF', 'Rand FC', 'Neural Classifier', 'Naives Bayes'],

'Crossval Mean Scores': [log_reg_mean, svc_mean, knn_mean, tree_mean, grad_mean, rand_mean, neural_mean, nav_mean],

'time':t_diff}

result_df = pd.DataFrame(d)

result_df = result_df.sort_values(by=['Crossval Mean Scores'], ascending=False)

result_df输出:

| Classifiers | Crossval Mean Scores | time | |

|---|---|---|---|

| 4 | Grad B CLF | 0.925765 | 26.047404 |

| 6 | Neural Classifier | 0.919359 | 82.371689 |

| 7 | Naives Bayes | 0.919359 | 0.207923 |

| 1 | SVC | 0.907706 | 71.862459 |

| 0 | Logistic Reg. | 0.905835 | 0.742473 |

| 5 | Rand FC | 0.886541 | 1.250071 |

| 2 | KNN | 0.829659 | 68.490700 |

| 3 | Dec Tree | 0.701087 | 1.155549 |

4.3 模型评价

由上表可以看出,在这8种分类器里面,梯度提升树(Gradient Boosting)、神经网络(Neural Classifier)、朴素贝叶斯(Naive Bayes)表现位于前三名。在后续的步骤中,我们可以对它们进行调参以获得更好的结果,相信大家一定会调参,所以调参不是本文关注的重点,本文的重点在于各个模型的比较。

虽然决策树位列最后一名,但是集成树(梯度提升树与随机森林)表现可以远远好于单棵决策树。这是由于集成模型的泛化性能非常好,不太需要调参就可以取得很好的效果。

而在耗时方面,k邻近算法由于要同时计算所有点与某点的距离,因此耗时最多,而且效果也一般(倒数第二)。集成模型虽然需要训练上百个弱分类器,但是由于可以并行计算的原因,随机森林与单棵决策树的速度相差无几;而根据梯度提升树的原理,它只可以分步计算,所以速度稍慢。但是最慢的还是神经网络,最快的模型是决策树。

#通过该函数获得一个分类器的AUC值与ROC曲线的参数

def get_auc(clf):

clf=clf.fit(X_train, y_train)

prob=clf.predict_proba(X_test)

prob=prob[:, 1]

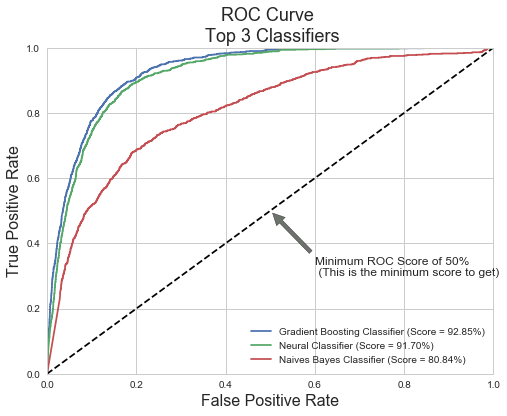

return roc_auc_score(y_test, prob),roc_curve(y_test, prob)通过测试集数据画出ROC曲线并标注AUC值。

grad_roc_scores,grad_roc_curve = get_auc(grad_clf)

neural_roc_scores,neural_roc_curve = get_auc(neural_clf)

naives_roc_scores,naives_roc_curve = get_auc(nav_clf)

grd_fpr, grd_tpr, grd_thresold = grad_roc_curve

neu_fpr, neu_tpr, neu_threshold = neural_roc_curve

nav_fpr, nav_tpr, nav_threshold = naives_roc_curve

def graph_roc_curve_multiple(grd_fpr, grd_tpr, neu_fpr, neu_tpr, nav_fpr, nav_tpr):

plt.figure(figsize=(8,6))

plt.title('ROC Curve \n Top 3 Classifiers', fontsize=18)

plt.plot(grd_fpr, grd_tpr, label='Gradient Boosting Classifier (Score = {:.2%})'.format(grad_roc_scores))

plt.plot(neu_fpr, neu_tpr, label='Neural Classifier (Score = {:.2%})'.format(neural_roc_scores))

plt.plot(nav_fpr, nav_tpr, label='Naives Bayes Classifier (Score = {:.2%})'.format(naives_roc_scores))

plt.plot([0, 1], [0, 1], 'k--')#指定x,y轴的坐标在0,1之间

plt.axis([0, 1, 0, 1])

plt.xlabel('False Positive Rate', fontsize=16)

plt.ylabel('True Positive Rate', fontsize=16)

plt.annotate('Minimum ROC Score of 50% \n (This is the minimum score to get)', xy=(0.5, 0.5), xytext=(0.6, 0.3), arrowprops=dict(facecolor='#6E726D', shrink=0.05),)

plt.legend()#显示图例

graph_roc_curve_multiple(grd_fpr, grd_tpr, neu_fpr, neu_tpr, nav_fpr, nav_tpr)

plt.show()

由上图可见,在测试集中朴素贝叶斯模型只得到了80.84%的AUC值了,说明它存在过拟合现象,需要进一步调参。而梯度提升树(Gradient Boosting)与神经网络(Neural Classifier)的得分与训练集的结果保持一致,说明模型拟合地很好,因此它们也是我们可以采纳的模型。

5、总结

首先,在营销活动次数的选择上,对同一个客户打电话的次数不应超过三次,这样不仅可以节约时间,把精力投入到新客户中。如果给同一个客户打电话多次,一定会引起客户的反感,从而降低客户的购买产品的欲望。

其次,在客户年龄段的选择上,银行应集中于20岁左右和60岁左右的人群,他们分别有超过60%的可能性购买营销产品。

再其次,对于不同的职业来说,学生与退休的人也是最容易购买营销产品的人,这与年龄段的现象保持了一致。对于退休的人而言,他们有很多的存款却不敢随便花钱,而定期存款大多期限短收益高,因而成为他们所热衷购买的产品。而对于学生党来说,他们会珍惜自己有限的存款,而同时他们花钱的机会比较少,所以他们会选择定期存款。

而对于住房贷款和存款余额来说,正如本文中的结果所能看到的一样,有贷款的人需要每月按时还款,因而不太可能还会去购买定期存款(定期存款的利息肯定不及贷款利息)。同时,存款多的人自然倾向于去购买定期存款以让自己获得更多利息。

最后一点,专注于那些通话时间长的客户,正如在关系矩阵中所看到的一样,通话时间越长客户越有可能购买营销产品,而且可能性非常之高。

综上所述,对于银行而言,想要推广它的营销产品,一个简要的策略是:首先先通过客户的基本信息,使用训练好的机器学习模型(不含duration)进行预测,然后对这些客户进行电话营销。根据电话营销的结果,再用含有duration的模型再一次进行预测,找出那些可能性大的客户,如果他们没有在第一次营销后购买理财产品的话,那么再对这些人进行第二次电话营销。之后,视情况进行第三次营销,或者把精力放在发展新客户上面。通过这样的策略,银行下一次营销活动的可能结果会比上一次更好。

跟着教程走了一遍,原来如此~

本博客所有文章除特别声明外,均采用 CC BY-SA 4.0 协议 ,转载请注明出处!